-

Home

-

Publications and submissions

-

Reports

-

EWON Insights

-

EWON Insights Oct-Dec 2021

- Energy complaints and case studies

Energy complaints and case studies

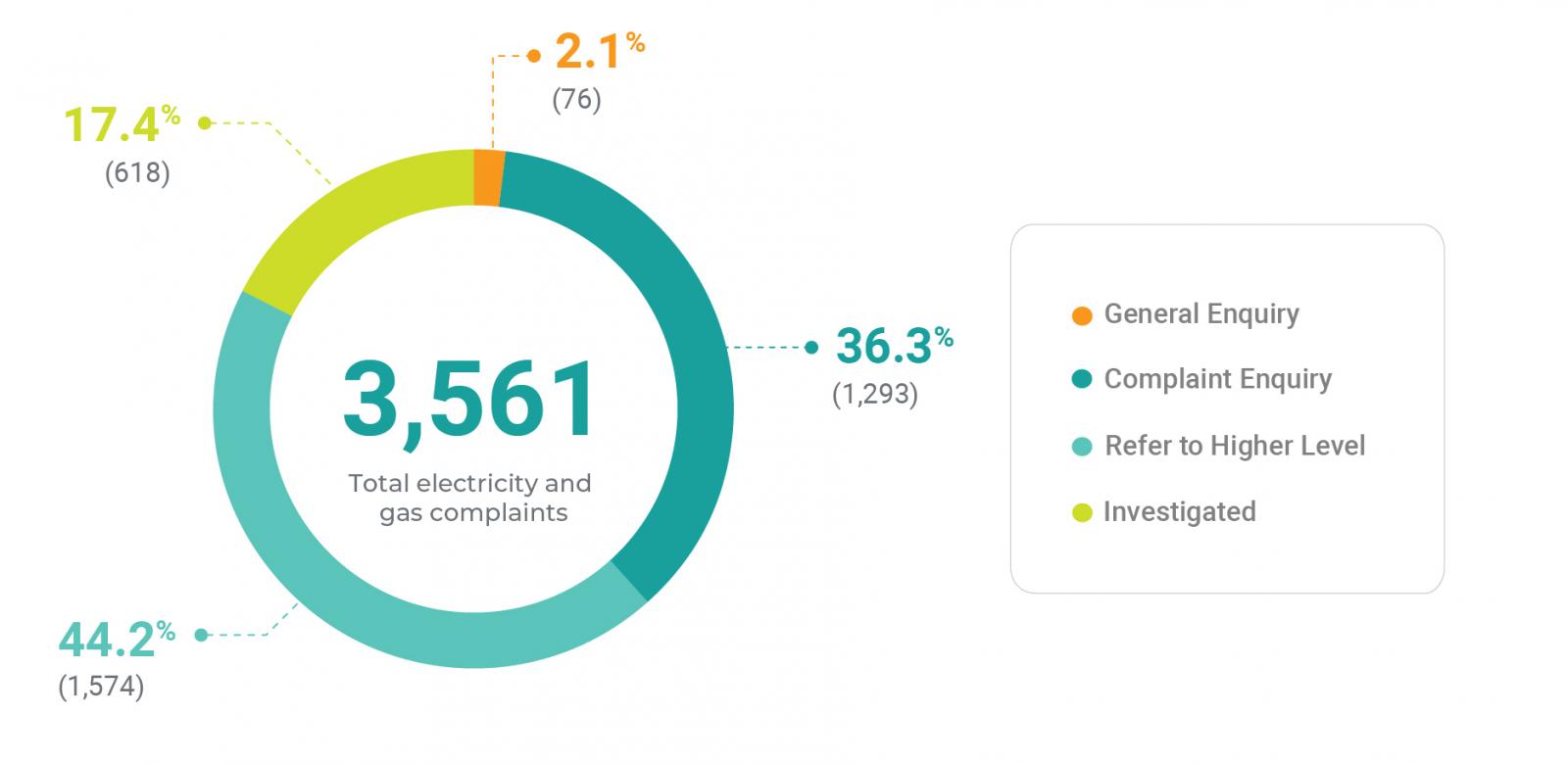

Table 4 – Energy complaint breakdown October to December 2021

| Complaint type | Number of complaints | % total energy complaints |

|---|---|---|

| General enquiry | 76 | 2.1% |

| Complaint enquiry | 1,293 | 36.3% |

| Refer to higher level | 1,574 | 44.2% |

| Investigated | 618 | 17.4% |

| Total | 3,561 | 100% |

Credit listing complaints

After billing and customer service, complaints where the core issue is credit are the second most common complaint EWON receives. A large proportion of these credit complaints are from customers disputing a default listed on their credit file. As debt moves through the collections cycle, a customer may be credit listed by an energy retailer if an energy debt remains unpaid and the energy retailer meets the required notice conditions. This is particularly interesting due to two current issues in the credit listing space.

- The Australian Energy Regulator’s (AER) Statement of Expectations (SOE) was lifted on 25 October 2021. The SOE set out expectations for energy retailers to provide extra protection and support to customers and the market throughout the COVID-19 pandemic. One expectation was that energy retailers defer referrals of residential and small business consumers to debt collection agencies for recovery actions or credit default listing. Energy retailers have now recommenced debt collection activity that can lead to credit default listing.

- The Office of the Australian Information Commissioner (OAIC) is conducting an independent review of the Privacy (Credit Reporting) Code 2014 (the CR code). This independent review is required every four years to decide whether and how the CR code could be updated. The OAIC is consulting with stakeholders for feedback on the CR code in early 2022. EWON will make a submission to this consultation, exploring issues raised by the credit listing complaints customers bring to us.

Credit repair agents

A significant portion of complaints to EWON about credit default listings involve commercial advocates, namely credit repair agents and solicitors offering credit repair services. For example, just over 25%, or 138 out of 535, of EWON complaints closed in the 2020-21 financial year where the main issue was a credit default listing were made via commercial advocates.

EWON has long raised potential issues with the use of commercial advocates by customers to assist with the removal of credit default listings. In September 2012, we published a report about a survey of EWON customers represented by credit repair agents, and mystery shopper research into credit repair agents. The report highlighted some common consumer circumstances and agent practices that were (and remain) of concern to EWON. In February 2021, the Australia & New Zealand Energy and Water Ombudsman Network (ANZEWON) made a submission to the National Consumer Credit Protection Amendment (Debt Management Services) Regulations 2021 Exposure Draft consultation. ANZEWON’s submission urged Treasury to consider better regulation of credit repair agents.

EWON’s concerns about credit repair agents include:

- credit repair agent fees can exacerbate consumer financial hardship, and are sometimes disproportionately high compared to the defaulted debt;

- credit repair agents are not generally equipped to deal with related issues like billing complaints;

- there is low awareness among consumers of free alternatives to credit repair agents, particularly among vulnerable groups such as Culturally and Linguistically Diverse (CALD) customers; and

- sometimes misleading conduct and/or incomplete information is provided to customers by some credit repair agents, including setting unrealistic expectations of the likelihood that a credit default listing will be removed.

When credit repair agents approach EWON on behalf of customers, EWON also sees some actions by agents that can hinder effective dispute resolution, such as:

- credit repair agents querying EWON’s procedures, particularly practices around ensuring customers are aware that EWON is a free alternative to the credit repair agent;

- EWON being unable to maintain contact with credit repair agents; and

- EWON having difficulty obtaining information necessary to progress investigations from customers when dealing with the credit repair agent as an intermediary.

Unlike credit repair agents, EWON provides a free service to customers seeking review of a credit default listing by an energy retailer. We set realistic expectations about the likelihood of removal and adhere to principles of transparency and procedural fairness. EWON is also well-placed to handle any other related aspects of a customer’s complaint, including concerns about customer service and billing. EWON’s work goes beyond each individual complainant. Credit listing complaints inform Policy work more broadly, such as making submissions to consultations related to the Privacy Act 1988 and the Privacy (Credit Reporting) Code 2014 to try to help improve the credit reporting system.

The following case studies illustrate the value EWON brings to reviewing credit listing complaints.

Case study: EWON assists in removal of default listing after customer pays credit repair agent

A credit repair agent contacted EWON on behalf of a customer who had a default listed on his credit file in December 2017 for an electricity account debt of $2,250. The customer was experiencing personal and financial hardship when the default was listed and considered the default listing unreasonable. The customer did not become aware of the default listing until over three years later, when he applied for finance. The customer had since paid the debt in full. The credit repair agent attempted to resolve the complaint with the energy provider, but the provider declined to remove the default listing. EWON referred the complaint back to the retailer at a senior level in the first instance. The credit repair agent returned to EWON and advised that the complaint was not resolved.

During the investigation, EWON confirmed that the customer was aware that as a free service, EWON could deal with him directly at no cost if he preferred. The customer advised that he had already paid $1,000 to the credit repair agent, with a further $500 payable if the default listing was removed. As he had already made a payment, he elected for the credit repair agent to remain his advocate for the EWON complaint.

The credit repair agent had raised several potential issues with the default listing, but EWON’s review indicated that none of these provided a reasonable basis for the default to be removed. EWON’s investigation identified that a portion of the $2,250 default amount was not overdue by 60 days when the default was listed. Compliant default listings require the whole amount of a debt be overdue by at least 60 days. On this basis, the energy retailer agreed to remove the default listing. EWON communicated the outcome to the customer, but he did not advise EWON whether he paid the additional $500 to the credit repair agent.

Case Study: Credit repair agent questions EWON’s processes

EWON was contacted by a credit repair agent on behalf of a customer who had a default listed on his credit file in October 2019 for an electricity debt of $1,500. He left the supply address due to the end of a relationship and experienced issues finalising the account in his name after his ex-partner remained at the property. He did not discover the default until over a year later, when he applied for finance. He considered the default listing unreasonable as he had not received any notices. EWON referred the complaint back to the retailer at a senior level in the first instance. The credit repair agent returned to EWON advising that the complaint had not been resolved.

EWON’s investigation was initially delayed due to issues obtaining confirmation that the customer was aware EWON’s service is free. There were also delays clarifying customer information via the credit repair agent.

EWON’s preliminary review did not identify a basis for the default to be removed. The credit repair agent then questioned the fairness of EWON’s dispute resolution processes and indicated he would tell the customer that it was EWON’s responsibility if the default was not removed. He also noted that if there was an unfavourable outcome, he would refer the customer to dispute this with EWON. We confirmed our independent role and explained that we are never able to guarantee removal of a default and would be happy to speak with the customer directly.

Although EWON did not identify any basis for removal and the retailer maintained that the listing was compliant, through the dispute resolution process the retailer offered to remove the default listing to resolve the complaint. The retailer made this decision in part because the customer had paid the debt in full, and the default listing was preventing him from obtaining crucial finance without which he would be in financial difficulty. EWON communicated the outcome and did not receive any further contact from the credit repair agent or customer.

Case Study: Removal of default listing leads to billing complaint being resolved

A customer advised that he had received an electricity bill of $2,800 from his retailer, which he considered to be high in comparison to his normal bills of $900 per quarter. The retailer confirmed he had been billed on correct actual reads and the disputed bill was payable. His account was closed when he changed retailers. Sometime later his broker advised him that he had a default listed on his credit file for $2,800 in January 2020. He contacted the retailer and requested it investigate the high billing further and review the default listing. EWON referred the complaint back to the retailer at a senior level in the first instance. The customer returned to EWON advising that the complaint was not resolved, this time requesting that we communicate with a credit repair agent as the advocate. The customer understood that EWON was a free service but did not wish to deal with the complaint.

EWON’s review of the default listing identified that the retailer had not used the customer’s preferred contact method to send the required notices before listing the default. The retailer removed the default listing on this basis.

EWON also investigated the underlying billing complaint, as the customer was still declining to pay the outstanding debt of $2,800. EWON’s review found that the disputed bill was for a winter period and had been based on actual reads. The retailer had arranged for a special meter read which was in line with the actual reads. At this point the customer had only had the account for a short period and did not have an earlier winter bill at that property for comparison. To facilitate resolution of the billing complaint, the retailer offered to apply a credit of $100. The customer accepted the $100 credit and indicated that he would pay the outstanding debt.

Case Study: Difficulty maintaining contact with advocate over default listing

A credit repair agent contacted EWON on behalf of a customer who had a default listed on his credit file in June 2019 for an electricity debt of $920. The customer disputed the default listing as the retailer did not update his address when he moved to a new address and closed the account. He also considered the retailer had not resolved a complaint he raised about being charged a move out fee. EWON referred the complaint back to the retailer at a senior level in the first instance. In return, the credit repair agent advised EWON that the retailer did not contact them in the agreed timeframe about the complaint.

The retailer advised that it had unsuccessfully attempted to contact the credit repair agent. EWON also had difficulty obtaining clarifying information and providing updates during the subsequent investigation, which further impacted the efficiency of the dispute resolution process.

EWON’s review did not identify a basis for the credit listing to be removed as the retailer had sent the required notices to the customer’s nominated email and contact records indicated the customer had been aware of the debt prior to the default listing. EWON’s review also indicated that the move out fee had been appropriately applied, and there was no information to support that the customer had disputed the fee at the time. EWON provided a detailed report about the outcome, and the advocate and customer were unable to provide any information to support further review.

Minimum amount for credit default listings

Since the implementation of the Privacy (Credit Reporting) Code 2014, the threshold for a default credit listing for overdue consumer credit has been $150.

With the increase in household expenditure, including rising energy costs over the last 10 years, this $150 threshold is disproportionate to the average bill or level of debt carried by an energy consumer. For example:

- The average debt from a customer entering a hardship program rose from $491 in the 2013/2014 financial year to $1,584 in December 20211

- The average annual gas bill in NSW is around $1,000 per annum for households using 24,000 megajoules (MJ)2

- The average electricity market offer in NSW produces an annual bill of $20083

In 2017, the AER confirmed that the disconnection threshold of $300 is effective in protecting customers and ensures customers are not disconnected for owing a relatively small amount.4

However, the AER is currently exploring whether stakeholders support the idea of a further disconnection threshold review in their Consumer Vulnerability Strategy consultation paper.5 EWON would support a threshold that is relative to the average bill.

Increasing the threshold for a default credit listing, to $300 or any amount set by the AER, in line with the disconnection threshold would be more relative to the actual cost of energy and go a long way to ensuring that customers who owe a small amount are not impacted significantly in the long term.

The current threshold is established in section 6Q(1)(d) of the Privacy Act 1988 and cannot be increased by amending the Code. EWON again calls on the Office of the Australian Information Commissioner and the Australian Retail Credit Association to consider consultation on this issue.

Alternatively, energy retailers could voluntarily adopt this threshold as an industry standard.

Case Study: Customer default listed for $266 after not receiving final gas bill

A customer moved out of a property in 2019 and contacted his retailer to close his gas account and provided a forwarding address for his final bill. The retailer did not update his forwarding address, so the final bill and notices were sent to an old address, where the customer no longer lived.

In October 2021, he checked his credit file and found the retailer had default listed him for $266 in September 2019. He contacted the retailer multiple times to request a copy of the final bill and any notices that had been sent to him, however the retailer did not provide this.

The retailer advised him that the default listing was appropriate and would not be removed. The customer told EWON he would have paid the bill if the forwarding address had been updated appropriately.

We referred the matter to the retailer for resolution at a higher level, informing the customer that he could return to EWON for further review and assistance if he was unable to resolve the matter directly with his retailer.

Case Study: Business customer contacted by collections agency for $219

A customer was contacted by their retailer to advise that there was an overdue amount of $219 on their electricity account. The retailer advised that the amount had originally been paid but was then refunded back to his business account. He reviewed several months of business transactions and provided copies of his bank statements to the retailer to show that no refund had been received, but the retailer sold the debt to a collections agency.

The customer was then contacted multiple times by the collections agency seeking payment of the amount. Although he provided a copy of his bank statement to the collections agency, he had not been able to resolve the issue.

He said that it was the second time that he had been contacted about the debt, even though he had paid the amount to the retailer directly after the first contact.

When EWON spoke to the customer’s retailer, it advised that it had received payment from the customer in February 2021—after the debt had been sold to the collections agency in September 2020. The retailer transferred the payment to the collections agency but then reversed the payment in its system, resulting in them contacting him about an overdue amount. The retailer reversed the amount owing, leaving the account with a nil balance, and confirmed that there was no outstanding balance on the debt collection agency’s file.

Duration of default disproportionate to debt level

A credit default listing is valid for a period of five years, regardless of whether the listing is for a debt of $150 or $30,000. Currently there is no leniency on the duration of a default listing, and a customer’s future financial stability and ability to obtain credit for things such as buying a house or starting a business are significantly impacted.

It is also possible to be default listed more than once for separate debts, such as separate electricity and gas accounts, at any one time. A customer trying to obtain credit may not be penalised further for having more than one default listed, however if defaults are listed at different times, the total period in which a customer is financially impacted will be longer.

If a customer holds dual energy accounts with one retailer, this could be addressed by either amalgamating the accounts into one debt or ensuring that the timeline of notices and default listing is the same.

Many of EWON’s cases are from customers who only find out they have a default credit listing when they apply for financial credit or loans, often years later. These customers often consider that they were not notified that they would be default listed, or they moved to a different property and did not receive the notification.

A default listing can be reviewed for compliance with the Code. However, this is stressful due to need for credit or time sensitivity, is onerous on a customer, and comes at a cost when using a credit repair agency.

The industry and regulators must consider and identify an approach that considers the amount of debt and whether it is appropriate to default list customers that owe a small amount or genuinely miss a payment. Below are some solutions that could address this issue.

Sliding scale of debt relative to length of default listing

In EWON’s submissions to the 2012 Review of the Credit Reporting Code of Conduct and 2017 Review of the Privacy (Credit Reporting) Code 2014 (v1.2) Consultation Issues Paper we supported the introduction of a sliding scale where the credit default listing is for a period proportionate to the amount of the debt.

For example, a debt of $1,000 or less would result in a one-year listing, a debt of $1,001 to$5,000 would incur a two-year listing, and debt of $5,001 to $10,000 a three-year listing. Debts above $10,000 would be listed for 5 years.

Industry-specific default thresholds needed

EWON recommends that different thresholds be set for different industries that are relative to the average consumer debt. For example, the average bill and debt in the telecommunications sector would differ from that in the energy sector and $150 may be more reflective of an average bill or build-up of debt over several months.

Changing the default threshold to be industry-specific would allow periodic review, taking into consideration changes in each industry, that would keep the default listing consistent with the industry whilst maintaining consumer protections.

Case Study: Customer default listed for gas and electricity accounts

A customer contacted EWON after he applied for credit and was declined due to two default listings by his previous energy retailer. He had been default credit listed for $326 for a closed gas account in June 2019 and $398 for his closed electricity account in October 2019.

He explained to EWON that he had ongoing significant health issues and had been impacted by COVID-19. He was not aware of any debt to the retailer and said that he always paid his bills on time, however had moved properties frequently due to his health concerns. When he became aware of the overdue amounts, he had paid the amounts in full.

EWON contacted the retailer and it advised that both debts had been sold to a collections agency but confirmed that the electricity account had been paid in full. It advised that there was still an outstanding amount of $86 towards the gas account. To help resolve the complaint, and taking into consideration the customer’s circumstances, the retailer offered to remove the default listing on the electricity account and remove the default on the gas account if the customer paid the remaining balance. The customer was happy with this resolution and advised that he would pay the outstanding balance on the account as soon as possible.

As the defaults were listed over 4 months apart, the case highlights that the customer would have been financially impacted for longer than 5 years for a dual fuel account. It also highlights that a customer is unable to obtain credit for a 5-year period for individual debts of less than $500 .

Final bills not received lead to debt collection

EWON receives complaints from customers who have a good payment history but do not receive their final bill after moving out of an address. We also hear from customers who have provided their email address only for the retailer to send the final bill to their last known postal address, which they do not receive.

Currently retailers send bills to a customer’s last known address, which may include sending notices via post to a physical address or electronically via email.

There is currently no requirement for retailers to attempt to contact customers via different methods, and customers can subsequently face debt collection action.

This apparent industry-wide communication issue allows for personal contact attempts and places protections on open accounts, yet falls short for customers closing accounts.

The National Energy Retail Rules (NERR) contain requirements regarding consent and information needed to open an account. These could be extended to account closures through:

- The requirement for retailers to obtain a forwarding address or email address in order to easily contact a customer and allow them to close an account or move out.

- The development of best practice industry guidelines to avoid default listing customers for missing a final bill when moving out or consider removal of a default if a customer can show their previous good payment history and continued payment history at a new property.

Rule 111 (1)(e) of the NERR requires retailers to use their ‘best endeavours’ to make personal contact either in person, by phone, fax or email. While contact by phone is standard practice for some retailers, a requirement to make personal contact with customers during the collections process would add another layer of protection for those customers not receiving notices.

Case Study: Customer didn’t receive overdue notices

An advocate contacted EWON and advised that the customer had been default credit listed in May 2019 for $259. At the time the debt had occurred, the customer was experiencing financial vulnerability and had been hospitalised for a period due to ongoing health concerns.

The customer became aware of the debt and paid the amount in full, and the advocate requested that the retailer remove the default because of the customer’s circumstances at the time of the default listing. The advocate also advised that the retailer had been unable to provide copies of notices sent to the customer.

The matter was referred to the retailer to review at a senior level in the first instance. However, the advocate returned to EWON as they were not contacted by the retailer.

When EWON contacted the retailer, it advised they had completed a further review of the matter and identified they had not updated the customer’s email address when the account was closed, meaning the customer was unaware of the default. The retailer confirmed the default listing would be removed.

Footnotes:

1 AER, Retail Market Performance Data Q4 2020-21

2 St Vincent de Paul Society – NSW Energy Prices July 2021

3 ibid

4 AER, Final Decision - Review of the Minimum Disconnection Amount – March 2017

5 Consumer Vulnerability Strategy, Draft for consultation paper - December 2021